PREVIOUS

✖

Pension schemes in India

January 9 , 2026

14 hrs 0 min

78

0

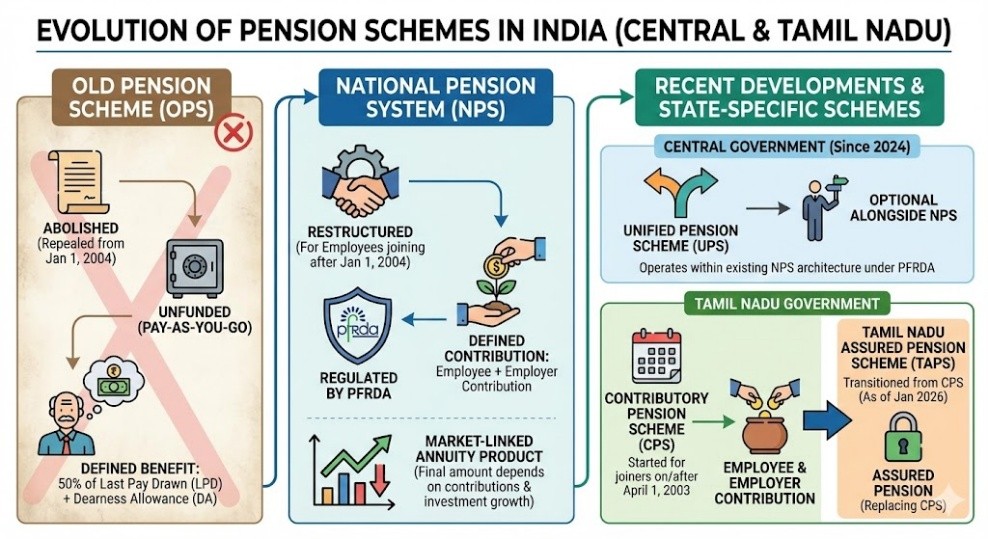

- The Old Pension Scheme (OPS) in India was abolished as part of pension reforms by the Union Government.

- Repealed from 1 January 2004, it had a defined-benefit (DB) pension of half the Last Pay Drawn (LPD) at the time of retirement, along with components like Dearness Allowances (DA), etc.

- OPS was an unfunded pension scheme financed on a pay-as-you-go (PAYG) basis in which current revenues of the government funded the pension benefit for its retired employees.

- The Old Pension Scheme was replaced by a restructured defined-contribution (DC) pension scheme called the National Pension System.

- The National Pension System (NPS) is a defined-contribution pension system in India, regulated by the Pension Fund Regulatory and Development Authority (PFRDA)

- The NPS started with the decision of the Government of India to stop defined benefit pensions for all its employees who joined after 1 January 2004.

- NPS is a market-linked annuity product.

- The Contributory Pension Scheme (CPS) was started in Tamil Nadu for those who joined service on or after April 1, 2003

- The contributory pension scheme is a retirement savings plan where both the employee and employer (or government/scheme provider) contribute funds regularly, often as a percentage of salary, into an individual account, with the final pension amount depending on total contributions and investment growth.

- As of January 2026, the Tamil Nadu government has transitioned from the standard Contributory Pension Scheme (CPS) to the newly announced Tamil Nadu Assured Pension Scheme (TAPS).

- The Unified Pension Scheme (UPS), introduced by the Government of India in 2024 as an optional pension scheme along with the National Pension System (NPS) for the Central government employees.

- UPS operates within the existing NPS architecture regulated by the Pension Fund Regulatory and Development Authority (PFRDA) and applies to both serving and retired employees under specific conditions.

Leave a Reply

Your Comment is awaiting moderation.