PREVIOUS

✖

Reconsideration on Fiscal Responsibility (Amendment) Bill, 2024

October 21 , 2025

7 hrs 0 min

13

0

- Tamil Nadu Assembly “rejected” Governor R.N. Ravi’s position on the need for the House to reconsider the Tamil Nadu Fiscal Responsibility (Amendment) Bill, 2024.

- It readopts the same bill without any changes.

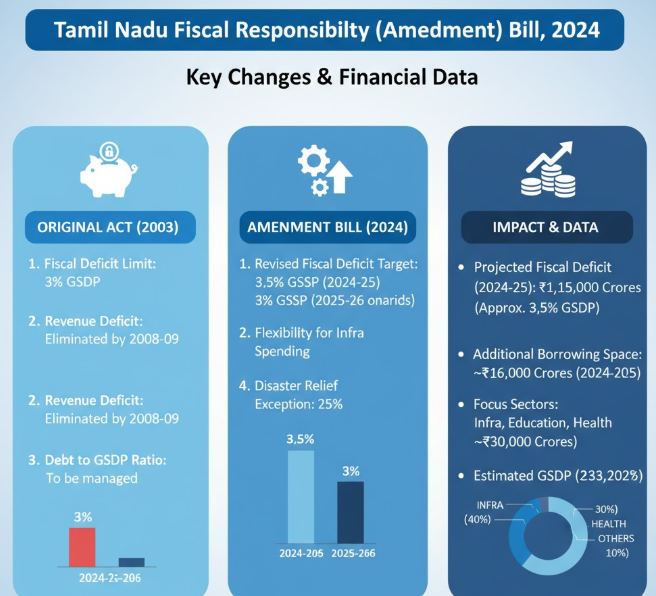

- The Bill seeks to postpone the achievement of zero revenue deficit and 3% fiscal deficit by another year.

- The Bill seeks to postpone the achievement of zero revenue deficit and 3% fiscal deficit by another year (now targeting 2026-27 and 31st March 2026 respectively).

- It is going beyond the period specified by the Fifteenth Finance Commission, which set targets for 2021-22 to 2025-26.

Governor’s Observations

- The next general election to the Tamil Nadu Assembly is scheduled to be held in less than a year from now.

- The proposed amendment will directly operate beyond the tenure of the present and into the tenure of the incoming government, effectively binding its fiscal policy choices in its very first year of office.

- It is also being beyond the recommended period of the Fifteenth Finance Commission.

- In a parliamentary democracy, it is a well-recognised convention that major policy decisions by way of statutory change, especially in the sphere of long-term financial policy, are ordinarily avoided in the immediate pre-election period unless there is a compelling necessity.

- This is to ensure that the newly elected government has the autonomy to determine its own fiscal framework in terms of the fresh mandate from the people.

- The original targets under the Tamil Nadu Fiscal Responsibility Act were enacted in alignment with the national framework for fiscal discipline under the Fiscal Responsibility and Budget Management (FRBM) Act, 2003, and successive Finance Commission recommendations.

- But the amendment proposed effectively altered the roadmap agreed with the Commission.

- This can threaten long-term fiscal sustainability and compliance with the targets outlined by constitutional bodies like the Finance Commission and potentially undermine the credibility of the State’s financial management.

- Fiscal responsibility laws are meant to be binding, and exceptions are usually made only in extraordinary situations (natural disasters, severe economic crises, etc.) by the elected government.

Leave a Reply

Your Comment is awaiting moderation.