PREVIOUS

✖

State and Trends of Carbon Pricing 2025

June 17 , 2025

16 hrs 0 min

36

0

- It was a World Bank report titled State and Trends of Carbon Pricing 2025.

- Carbon pricing instruments capture the external costs of greenhouse gas (GHG) emissions.

- These external costs—such as damage to crops, healthcare expenses from heat waves and droughts, and property loss from flooding and sea level rise—are typically borne by the public.

- Carbon pricing mechanisms tie these costs to their sources, usually through a price on emitted carbon dioxide (CO2).

- The report covers three types of carbon pricing instruments: Emissions trading system (ETS), carbon taxes and carbon credit trading mechanisms.

- An ETS involves governments setting a limit, or cap, on the amount or intensity of GHG emissions generated by emitters.

- Companies are allowed to trade emission units to meet their targets.

- If they implement internal measures to lower their emissions, they can sell these units to other emitters.

- A carbon tax explicitly prices carbon by defining a tax rate on GHG emissions or the carbon content of fossil fuels.

- Governments can levy this fee on companies for their GHG emissions.

- A crediting mechanism allows the trading of credits (each representing 1 tonne of carbon equivalent) generated through the activities that reduce emissions (e.g., capturing methane from landfills) or remove them (e.g., sequestering carbon through afforestation).

- Companies can then purchase these credits to offset their own emissions.

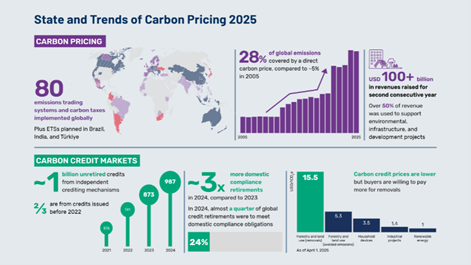

- Countries are increasingly adopting carbon pricing, which now represents almost two-thirds of global Gross Domestic Product.

- The number of operational carbon pricing instruments has grown significantly, from 5 in 2005 to 80 today.

- India, Brazil, and Türkiye are actively developing them.

- The Carbon pricing instruments now cover approximately 28 per cent of global GHG emissions.

- The report noted that most new and planned instruments are ETSs.

- India’s ETS will be rate-based, meaning emissions are not capped.

- Instead, emitters are allocated a performance benchmark that serves as a limit on their net emissions.

- Among the different sectors, carbon pricing coverage was highest in the power sector, followed by the industry, mining and the extractives sector, buildings, land transport and aviation.

- However, waste and agriculture are largely not covered by carbon pricing.

- The national determined contributions is a country’s demand for or international carbon credits under Article 6 of the Paris Agreement to meet national climate targets.

Leave a Reply

Your Comment is awaiting moderation.